Quarterly Investment Update March 25

“It’s the economy, stupid” - a phrase coined by Bill Clinton’s team when summing up what matters to US voters. Fast forward to today, and Trump’s ‘America first’ approach is ironically hindering economic growth.

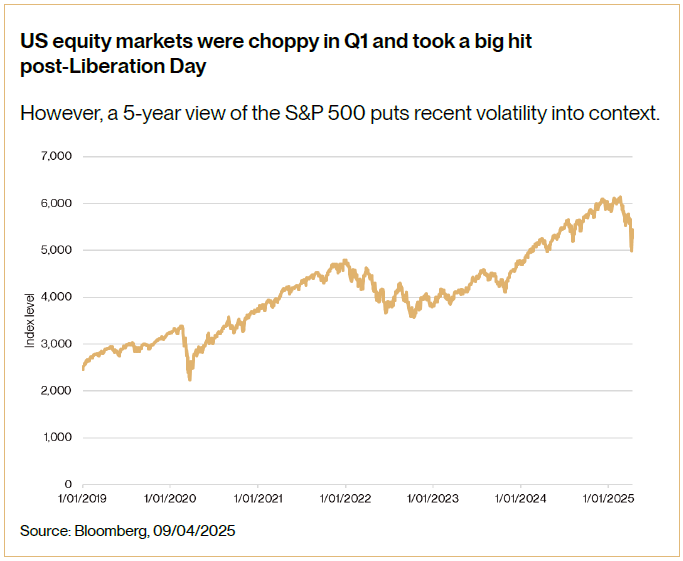

It has been a volatile start to the year, largely (but not exclusively) thanks to an unpredictable President Trump and his fondness for punitive trade tariffs.

Rising uncertainty and fraught geopolitical tensions, as well as supply chain friction and renewed inflationary pressures, have combined to create a foggy short-term environment for investors. Nonetheless, the case for long-term investing remains compelling.

In March, Trump’s decision to slap a 25% tariff on all aluminium and steel imports was swiftly counter-punched by both the European Union and China. The former jabbed back with tariffs to the tune of US $28 billion on US goods, while the latter landed a 10-15% tariff blow on US farm goods.

Almost immediately after Q1 closed, Trump announced sweeping new tariffs on a day dubbed “U.S. Liberation Day” (2nd of April), marking a significant shift in global trade dynamics. A blanket 25% tariff has been imposed on all foreign-made vehicle imports, alongside a 10% tariff on most foreign goods, and a 20% tariff on imports from the European Union. The US President claimed the measures would catalyse US $6 trillion in domestic investment.

The new tariff regime introduces a 10% base rate, with higher levies targeting specific countries: 34% on Chinese goods (latterly escalated to 125%), 20% on Japanese imports, and a substantial 46% on products from Vietnam. Negotiations with Canada and Mexico are ongoing.

In response, and reflecting investor concerns about trade frictions and economic headwinds, the U.S. Dollar Index reversed all of its post-election gains. Global markets also reacted sharply, particularly in the technology and automotive sectors, where investors had anticipated exemptions or sector-specific carve-outs.

The tech-heavy S&P 500 Index fell over 10% in the two days following the announcement, and entered correction territory. With or without a pugnacious US President, the stellar run seen in recent years - largely fueled by the so-called ‘Magnificent 7’ stocks such as Apple, Meta and Nvidia - had to come to an end sooner or later.

Tellingly, the Cboe volatility index - often referred to as the VIX, and seen as a ‘fear gauge’ for the S&P 500 – spiked to a level of 52 in the aftermath of the tariff announcement. While the surge was noticeable, it wasn’t the worst spike to be recorded in recent years. For context, both the Global Financial Crisis (GFC) in 2008, and the declaration of the COVID-19 pandemic in 2020, pushed the VIX into 80-level territory.

When quizzed by journalists on the tariff turbulence, Trump failed to rule out the possibility of a US recession in 2025. It was a startling position given how Presidential reputations are famously staked on the health of the economy. It also highlighted how quickly the mood deteriorated across the quarter. Only a few months beforehand the focus had largely been on the US economy’s ‘soft landing’.

In parallel, the energy-sapping battle to dampen inflation rumbles on, with tariffs blamed for re-stoking the embers. Renewed price pressures brought on by tariffs have dented early optimism for a significant downward trajectory (of inflation) in most key economies. Current estimates point to the effects of tariffs potentially raising household inflation by up to 0.7 percentage points.

In January and March, the US Federal Reserve (FED) opted to keep the Fed Funds Rate at 4.25% to 4.5%. A similar story played out across the Atlantic, where the Bank of England kept its base rate on hold at 4.5%. Both central banks aim for an inflation target of 2%, and both blamed emerging global uncertainty for their reluctance to trim rates.

The Fed now finds itself at a crossroads. The fear that tariffs will feed inflation runs parallel with forecasts suggesting they’ll shave up to 1% off U.S. GDP growth in 2025. Against that backdrop, the central bank may hold-off future rate cuts while it assesses the economic fallout. Or it could decide to look through a one-off spike in inflation and re-start monetary easing in an effort to salvage a weakening US economy. In this context, fixed interest allocations - especially those positioned for rising volatility or disinflationary pressure - could play an increasingly important role in overall portfolio resilience.

Meanwhile in China, the world’s second largest economy, problems persist as shrinking domestic consumption and a stuttering property sector take their toll. However, initial data releases painted a relatively encouraging picture of the first three months of the year.

Towards the end of the quarter, the Chinese government announced sweeping measures to “vigorously boost consumption”. The latest round of stimulus was a big statement of intent as the government pursues a GDP growth target of 5%. The measures included plans to issue $179 billion worth of special treasury bonds in 2025.

Chinese rhetoric against the US also ramped up, with tariffs and Taiwan proving to be recurring sources of tension.

All-in-all, this uncomfortable backdrop triggered a flight-to-safety for some investors, with noticeable in-flows to perceived safe-haven assets. Soaring demand for gold saw the price of a single ounce breach the $3,000 mark in April. In parallel, it was reported that over $20 billion poured into shortterm US debt. Given the numerous global challenges, a heightened investor appetite for portfolio/fund safety may endure in the coming months.

Conflict remained a big catalyst for news flow across the quarter, with differences of opinion about the conclusion of the Ukraine-Russia war driving a wedge between the US and Europe. Matters were made worse by the leaking of highly sensitive military-level discussions over Signal, which revealed less-than-favourable US opinion of European allies.

Europe’s leaders are now scrambling to bolster their defence plans in anticipation of reduced support from Washington. In a significant development, politicians in Germany passed a law that radically alters the borrowing rules in one of Europe’s key economies. From now on, German defence and security spending is exempt from borrowing limits.

Back in New Zealand, the quarter closed on an upbeat note with the news of an economic bounce back. The March data-release for NZ Gross Domestic Product (GDP) showed a 0.7% rise for Q4 2024. GDP per capita was up (by 0.4%) for the first time in two years. The recession is technically over but doubts remain over the sustainability of the uptick.

In February, the Reserve Bank trimmed the OCR to 3.75% (from 4.25%), linked to Q4 2024 inflation sitting at 2.2%. In a surprise turn of events, the rate cut was followed by the mid-term resignation of Governor Adrian Orr.

Across the Tasman, and in one of the closing acts of the quarter, Australians were given a federal election date of 3 May.

In summary

The first three months of 2025 generated dramatic news headlines as tariffs, conflicts and widespread uncertainty were catalytic for short-term turbulence in financial markets.

As the world continues to adapt to the sudden upheaval of global trade, more short-term volatility is to be expected, especially in global risk assets tied to emerging markets and export-oriented sectors.

For investors, it is imperative not to panic. Whilst history is never a guarantee of future performance, a look back in time shows that no politician - regardless of how loud their bark might have been - has ever negatively impacted global markets over the long term. Ultimately, markets will always dance to the beat of their own drum. And it pays to remember that uncertainty can also create opportunity.

For those investors who stay calm and maintain diversified holdings over the long term, the odds of securing positive returns remain firmly stacked in their favour.

Read the full report here