Q2 Quarterly Investment Update

The second quarter of 2025 was breathless for investors, with the White House serving up a politically undercooked menu of trade policy posturing and flip-flopping. Events in the Middle East also took a worrying turn. The global economy and financial markets came up against strong headwinds.

On the positive side, inflation pressures continued easing in key economies, with interest rates - a painful post-COVID handbrake on growth - now on a firm downward path and for some economies, approaching the end of their interest rate easing cycle.

The Reserve Bank of New Zealand (RBNZ ) cut our Official Cash Rate (OCR) by -0.25% in both April and May reducing it to 3.25%. The Reserve Bank of Australia (RBA) held their rates steady in April, before trimming a little in May to 3.85%. The European Central Bank (ECB ) also followed suit in June to 2.15%, which could be their final rate cut as inflation looks beaten in the Eurozone area.

However, central bankers continue to focus on the uncertainty of the impact of US trade tariff policy, particularly regarding increased inflation risks and lower economic growth prospects. For that reason, the US Federal Reserve (Fed) decided against cutting rates further in May and June, leaving them at 4.25%–4.50%, and much to the annoyance of Trump who sees them as too restrictive.

An allergic reaction to the so-called ‘Liberation Day

In April, equity markets had an allergic reaction to the so-called ‘Liberation Day’, when the White House unveiled its true intentions for global trade. To the consternation of many, the tariffs were extremely punishing, even for countries considered as allies.

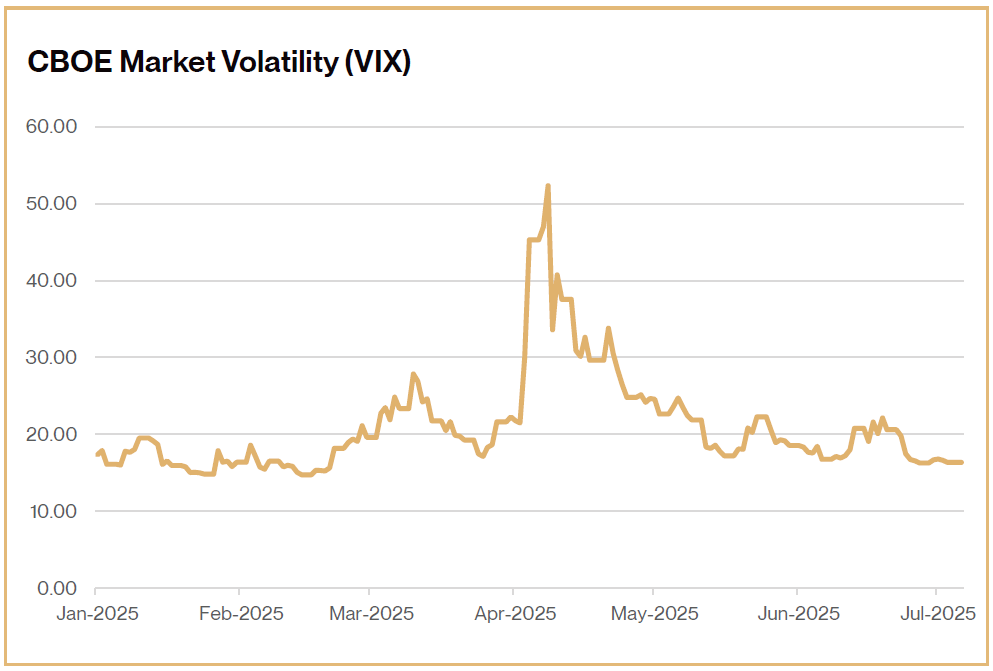

In response, markets fell sharply. The CBOE Volatility Index (see page 5), commonly known as the VIX and considered an investor fear gauge, surged above 50 (from a level of 17) early in the month, and the highest since the pandemic, before retreating to sub-20 in May.

By May, there were signs that US trade policy aggression was thawing and markets reacted favourably. Confirmation of a bilateral US-UK trade deal at the start of the month, was followed by independent temporary tariff reprieves for both the Eurozone and China. The phrase, ‘TACO’ - Trump Always Chickens Out - quickly spread across Wall Street, and the prospect of lower eventual tariff rates, than first feared, buoyed markets.

Investor sentiment also rose off the back of a judicial challenge to Trump’s ability to enforce tariffs in such a manner. However, in a sign of the yo-yo nature of today’s tariff news, the month ended with Trump’s announcement that steel and aluminium tariffs would double to 50% (effective from 4 June).

A few weeks later, it was revealed that the US and China would meet in London in June for trade talks that appeared to yield a fragile truce. Amid the turmoil, the standout stock news came via Nvidia. With quarterly revenue reported at over $40 billion, the hype surrounding the AI chip maker, as well as the overall trend of AI more broadly, continues to grow at pace.

More broadly, US equities now look expensive relative to other geographies, and some rotation away from them could be expected through the remainder of the year. Even more so if current levels of uncertainty and unpredictability weigh on the US economy. As an example, allocations to European equities may subsequently pick up, even if the current relative outperformance (year-to-date) versus the US equities loses steam later in the year.

Bond markets wobbled

Bond markets also wobbled during the quarter. US Treasuries - an informal benchmark for global government debt - sold off sharply in reaction to ‘Liberation Day’. The current climate has dented their attractiveness, fueled by higher-for-longer US interest rates, inflation uncertainty (linked to tariffs) an opaque economic growth outlook and concern over the ever-growing debt level of the US with no clear plan to reduce it. Some investors sought out other territories in the quarter, with Asian and European bond markets benefiting from those investors keen to diversify away from the US.

Geopolitical tensions remained a key source of market uncertainty during the quarter, despite pockets of encouraging news for investors. Efforts to negotiate a ceasefire between Russia and Ukraine faltered, and the Middle East witnessed a sharp escalation in hostilities late in the period.

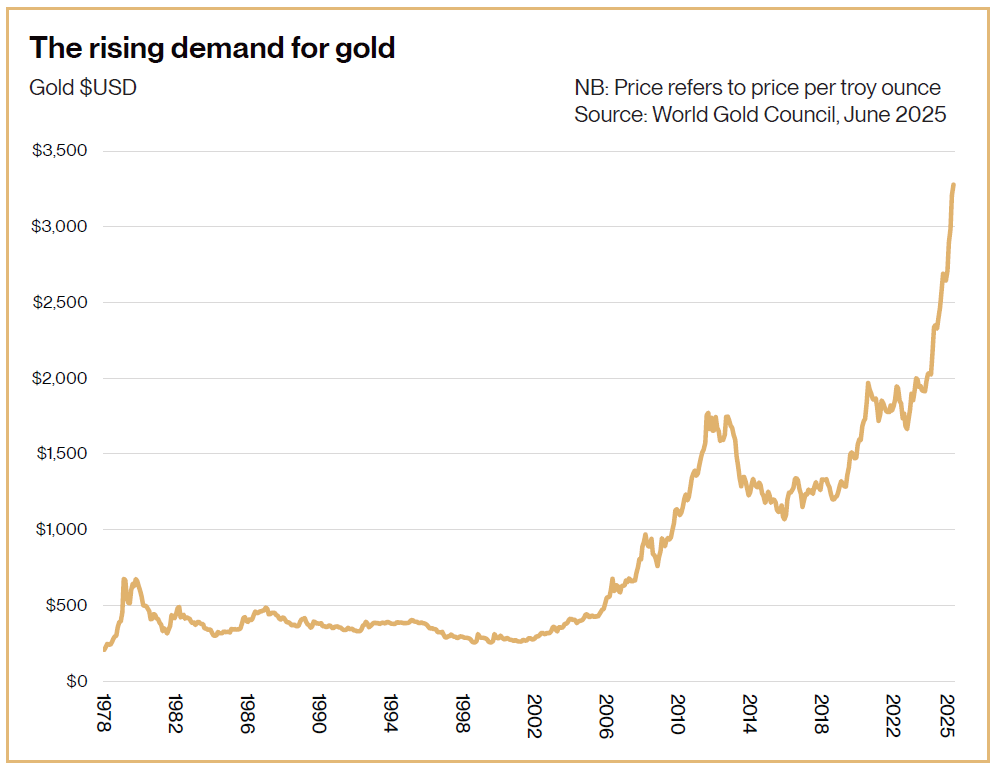

Israel conducted unilateral airstrikes on Iran’s nuclear infrastructure, prompting swift retaliation from Tehran. In a surprise move, President Trump ordered direct US strikes on Iranian nuclear facilities, a dramatic intervention that unsettled markets. Gold, already well bid through the quarter, spiked above USD $3,430 per troy ounce, an all-time high. However, the initial spike in oil prices quickly reversed, falling by $10 in the days following the strikes.

This was partly due to the limited nature of the attacks and the absence of any immediate disruption to oil supply or shipping routes. While equity markets initially sold off, sentiment stabilised as investors reassessed the risk of broader regional conflict. Nonetheless, the potential for further escalation remains a key tail risk heading into the second half of the year.

US Treasuries initially rallied, with 10-year yields briefly touching 4.30%, but inflationary fears from higher oil prices caused a late-session reversal, ending the week higher at 4.40% and finished the quarter at 4.23%. The episode underscored the fragility of investor confidence in a macro environment already strained by trade friction and added another layer of complexity to the Fed’s already cautious monetary policy stance.

Gold demand rising

Unsurprisingly, the strong investor appetite for gold kept its price above the US$3,000 mark (per troy ounce) throughout Q2.

Conversely, the US dollar - historically considered a ‘safe haven’ asset - further weakened since the start of the year. By the end of June, it was down

10.7% since the start of the year. Likewise, the appeal of US government debt, a common asset-of-choice for portfolio ballast, started to wane in the face of mounting debt fears.

In a stunning turn of events, the CEO of one of America’s largest banks - Jamie Dimon of JP Morgan - publicly opined that the US debt burden was unsustainable. His concerns were fuelled by the prospect of Trump’s spending through even further debt – his ‘Big Beautiful Bill’. In an effort to reassure investors, US Treasury Secretary, Scott Bessent went on national television in June and stated that the US would never default on its debt obligations.

History shows that criticism of White House policy rarely ends well. In June, Elon Musk announced that he was stepping away from his political role. He then swapped brutal insults with Trump over social media. So bad was the fallout, that at one point, Tesla’s market value had plunged by $150 billion.

Musk has subsequently said he plans to start his own political party named the ‘America Party’. There was calmer news closer to home. The Australian federal election victory of Labour’s Anthony Albanese put Australia’s long running political uncertainty to bed.

New Zealand market

Meanwhile in New Zealand, the government unveiled its latest Budget on 22 May releasing an accelerated tax depreciation policy to encourage business investment, additional investment in health, education, law and order, and other frontline public services, new infrastructure spending (including hospitals and schools), targeting low income family support and some changes to KiwiSaver contributions - both at an employer, employee, and government level.

New Zealand’s post-recession recovery also held up across the quarter. In the view of the RBNZ, the domestic economy is slowly moving in the right direction with lower borrowing costs and an expected recovery in the jobs market. There is better agricultural growth, education services demand and improving inbound tourism while construction, retail and services remain constrained.

In summary

The quarter will be remembered as highly volatile but nonetheless provided positive returns for portfolios. Equity markets and bond markets showed their sensitivity to trade tariff uncertainty, as well as their appetite for reconciliation amongst global trade partners. The swift recovery in the aftermath of April’s ‘Liberation Day’ dip, was positive news for those investors who held their nerve and didn’t panic sell when markets fell. Markets also had to grapple with a sharp escalation in Middle East tensions, which reinforced risk-off sentiment and drove spikes in gold and volatility in oil prices.

For all of Trump’s posturing, the reality is that there are few winners from a deteriorating trade environment. The mid-term elections in early 2026 will provide a potential finish line, by which time one might assume that deals will have been struck, and relative harmony restored. Under that scenario, Trump could spin a positive story to US voters.

As always, the key for investors remains in holding diversified assets and investing for the long term. Short-term news events don’t determine our investment philosophy.

---

If you would like to read the full report, please contact one of our advisers.