OCR drops to 2.25%

For the second time in a row, and for the last time with Christian Hawkesby at the helm, the Reserve Bank’s Monetary Policy Committee (MPC) has voted to reduce the Official Cash Rate (OCR).

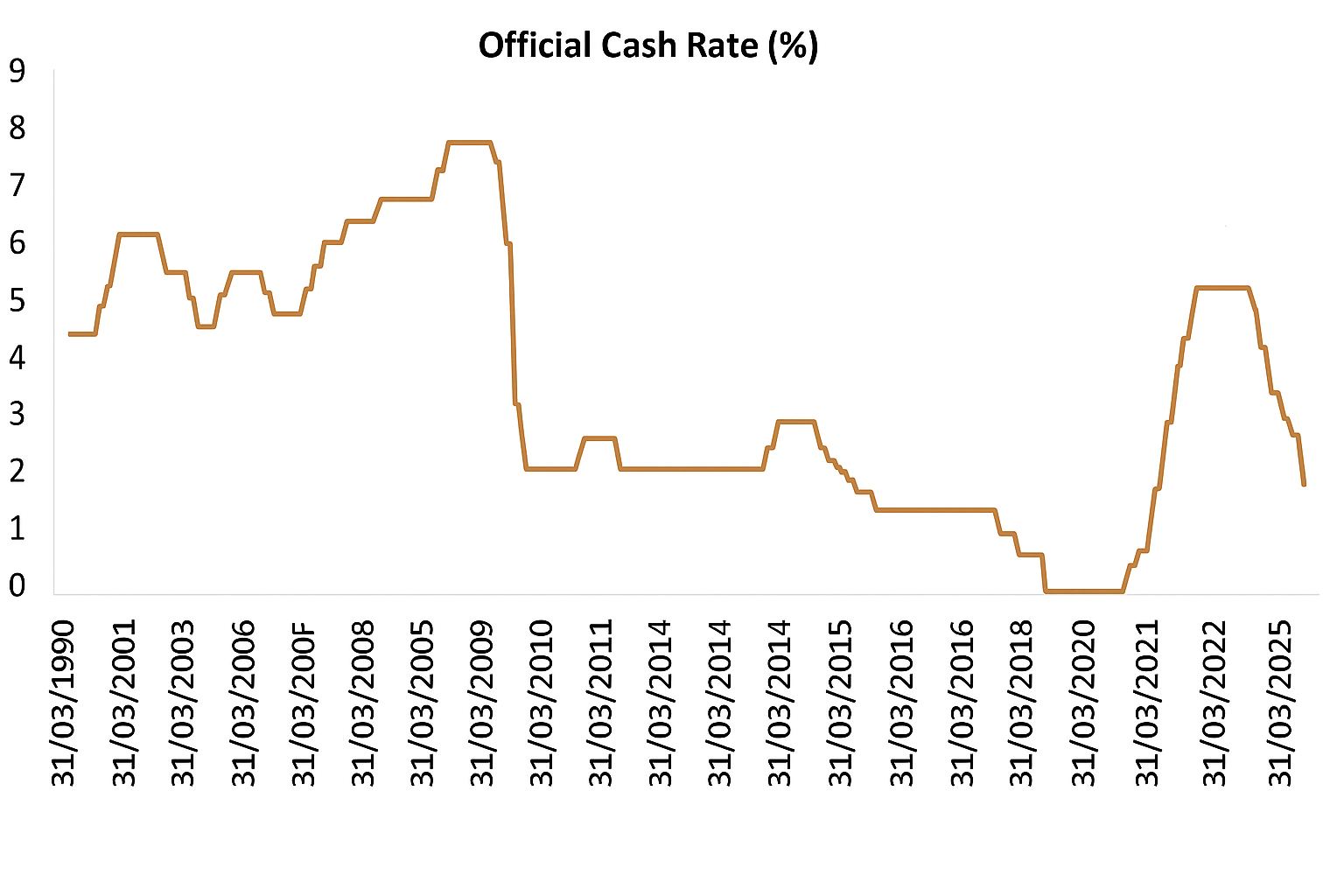

Following a 25bps haircut, the new OCR is 2.25%. For context, the last time the OCR was below 2.5% was in late July 2022[1].

Two in a row

Despite green shoots emerging in some parts of the NZ economy, the pace of the post-recession recovery has made for a hard watch.

Frustrated by the snail’s-pace progress, and eager to shake off the lingering sense of fragility, MPC members were highly unlikely to opt for anything other than a cut.

The MPC’s increasingly dovish stance was further confirmed by post-meeting comments that pointedly left the door open for future cuts should the economy need them.

Green shoots vs. inflationary pressures

The fact that the latest reduction was half the size of the one in October tells its own story.

On the one hand, the RBNZ wants to inject some vim and vigour into a slow-grinding economy. On the other hand it’s weary that domestic inflation is at the top end of its 1-3% target.

Given the lag between policy announcement and policy impact, there’s also a waiting game to be played as the cuts work their way through the various layers of the economy. The risk being that deeper and faster cuts at this stage could be premature and counterproductive. Hence, the smaller 0.25%cut this time around.

As Bevan Graham, Chief Economist at our Salt Funds division explains, overall inflation concerns have abated despite price pressures running hot again: “While the CPI was nudged to 3% in the year to September, we don’t think it will go higher. This is now in peak territory, and the path to lower inflation has been well laid. Against this backdrop, the MPC felt that it had licence to cut now without re-stoking the inflation fire. That said, our current view is that interest rates will need to rise again from early 2027 to keep inflation in check as the economic recovery strengthens.”

Happy new year?

For incoming Governor, Dr Anna Breman, the next MPC session – which will be her first official one – is not until 18 February 2026.

By the time this rolls round, there should be more clarification about whether the October and November cuts have done their jobs.

Judging by the early signs, the October reduction was indeed catalytic. The NZX50, for example, has ridden a wave of lower rates and improved valuations, reaching fresh highs this month.

As Bevan explains, there are glimmers of hope that the new year will bring better fortunes for Kiwis: “While it’s too early to pop the champagne corks, there is room for cautious optimism. A few structural issues continue to hold the NZ economy back but there are more bright spots on the horizon. It looks like we are past the worst in the labour market, and the recent small uptick in consumer spending could be a sign of what’s ahead. There are still risks worth keeping a close eye on but in terms of optimism, we think the glass is more than half full.”

Keeping you informed

The latest rate cut is welcome news ahead of the festive season. If it does what it’s intended to do, then Kiwis can afford to have a more positive outlook than the last 12 months have afforded them.

For borrowers, 2026 could be a good year for locking in lower rates before they potentially rise again in 2027.

As important as it is to monitor domestic monetary policy, the reality for global investors is that next month’s rate decision by the US Federal Reserve is of much bigger significance.

The Fed’s decision-making will influence the direction of the US economy, and in turn, the appeal of US assets – both of which are worth keeping an eye on in the context of well-diversified, globally structured portfolios and funds.

For New Zealand borrowers, a lower OCR should go down as a ‘win’ after many months of putting in some hard yards.

As ever, we’ll keep you informed about latest market themes and trends. Our ‘Market Insights’ article for November will publish shortly, as will our new ‘Outlook 2026’ report.

For any queries specific to your investments with us, please do contact your Adviser directly

[1]Source: https://www.rbnz.govt.nz/monetary-policy/monetary-policy-decisions

Photo credit: David St George