New OCR, new hope for the NZ economy?

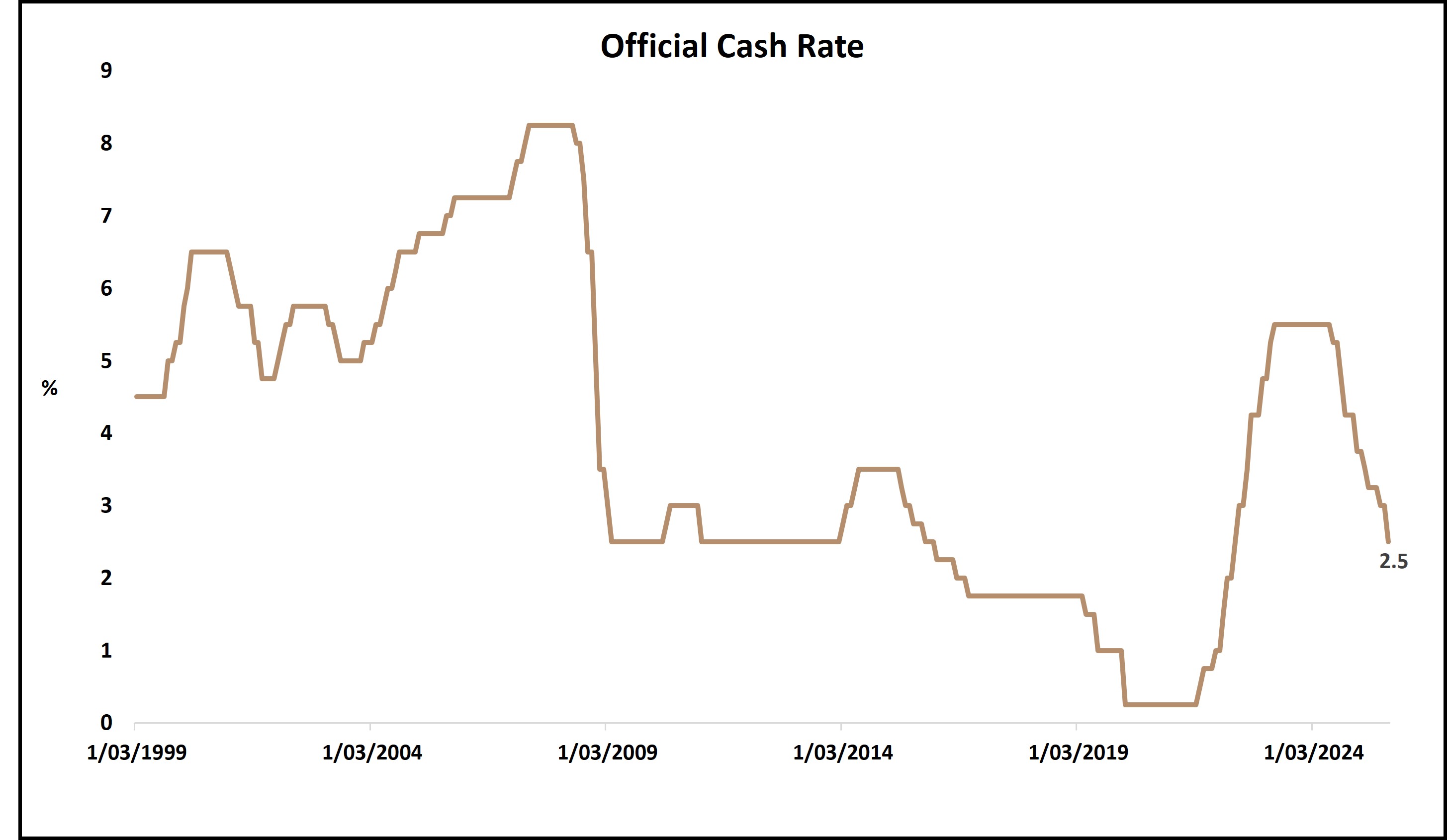

The Reserve Bank of New Zealand has trimmed the Official Cash Rate (OCR) by 50 basis points, taking it to 2.5% - the lowest it’s been since July 2022[1].

In doing so, the RBNZ has acknowledged the limp performance of NZ’s economy in 2025, and it will hope to have set the wheels in motion for a sustainable period of growth.

On current form, there are enough economy-related concerns to suggest that further cuts may be needed. The incoming central bank Governor, Dr Anna Breman, will certainly be under no illusions of the challenges that await her when she starts her 5-year term on 1 December 2025.

Hoping for a revival

Overall, a lower OCR is welcome news. The ongoing sluggishness of the Kiwi economy made it a relatively clear-cut case that a significant cut was coming.

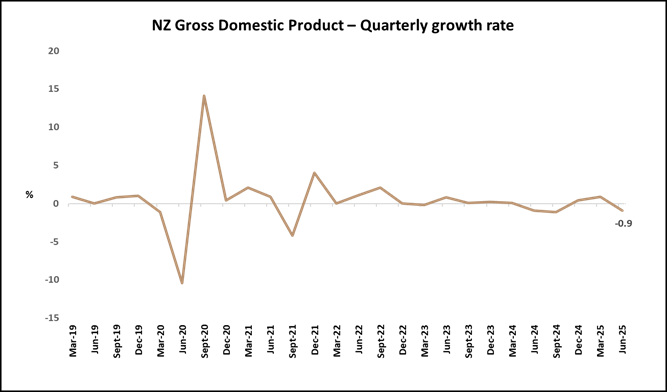

With the most-recent GDP data showing a worse-than-expected contraction of 0.9% for the June quarter, it all-but-confirmed that the central bank had to deliver more than a 0.25% cut.

All in all, it’s not a good backdrop for the Coalition government or the policymakers at the Reserve Bank, amid stubborn inflation, relatively high unemployment, and an ongoing talent exodus. Over 73,000 New Zealanders emigrated over the past year, according to recent reports[2].

As the RBNZ stated following its meeting: "Economic activity through the middle of 2025 was weak. In part, this reflects domestic constraints on the supply of goods and services in some industries, and the impact of global economic policy uncertainty. Household consumption is recovering, partly because of lower interest rates, and elevated commodity prices continue to support the primary sector. House prices are flat, and residential and business investment remain weak [3]".

For context, New Zealand’s challenges aren’t unique. Central Bankers around the world are under pressure to cut rates despite inflation refusing to trend down at a quicker rate.

In the US – the world’s most important economy – the issue is acute. In case you missed it, we covered this and more in our September edition of ‘Market insights’.

Implications for personal finances

From a financial planning perspective, the anecdote – one swallow doesn’t make a summer – comes to mind. If you’re already following a suitable long-term financial plan, then a single rate change by the Reserve Bank shouldn’t really change anything.

That said, there are potential implications for savers, investors, and borrowers that are worth being aware of.

On the one hand, the cut will be good news for borrowers, assuming it is passed down the chain by lenders, and helps to reduce borrowing costs. Business owners may also welcome the opportunity to borrow at a cheaper rate and invest back into their firms, which could boost capital spending and hiring, amongst other things.

On the flip side, and broadly speaking, a rate cut bodes less well for savers and those relying on Term Deposits (as an example), as it reduces the expected return for taking little risk.

In parallel, rate cuts can strengthen the case for investing. This is because, when faced with less favourable cash-based solutions, it may make sense to allocate a portion of your surplus cash into investments –where it has the potential to achieve higher returns, subject of course to your personal circumstances and tolerance to risk.

Some questions worth pondering

Ultimately, the formation and success of a long-term investment strategy involves working with your Adviser to identify the options that best match your unique objectives and circumstances.

With that in mind, here are some questions that you might like to explore:

- In the current rate environment, am I comfortable sitting on surplus cash? Or am I being too conservative?

- Can I use cheaper borrowing to restructure my debts, and/or pay down a loan faster than I was intending?

- Would moving some of my surplus cash into my portfolio align with my longer-term objectives?

- Is my property ownership doing what I intended it to do? Am I too reliant on real estate for my estate’s wider investment goals?

- Have any personal circumstances changed in the last 6-months? And would I benefit from having a chat with my Adviser about them?

Some final thoughts

The reduction to the OCR was expected and has been well received. New Zealand’s economy needs a leg-up in the tail-end of a difficult year, and efforts to catalyse it are welcome.

The challenge, however, remains how to inject some much-needed licence-to-grow, without bumping inflation back up. There’s also the ongoing trade uncertainty linked to US tariffs to contend with.

There is one more monetary policy meeting before Dr Breman takes up her post. Looking at NZ’s economy throughout this year, it wouldn’t be a huge surprise if there was another rate cut before Christmas – potentially a timely present for Kiwis to take into the holiday season.

The information provided in this article is for general information purposes only and does not constitute financial advice. We recommend that you seek financial advice from a qualified professional before making any financial decisions.

[1] Source: https://www.rbnz.govt.nz/monetary-policy/monetary-policy-decisions

[2] Source: https://www.stuff.co.nz/nz-news/360819173/number-people-leaving-nz-increase-latest-migration-figures-show

[3] Source: https://www.rbnz.govt.nz/hub/news/2025/10/ocr-reduced-to-2-5-percent

Photo credit: www.christchurchnz.com