Is a big market correction coming?

Please note, all data below has been sourced and verified via Bloomberg unless stated otherwise. Past performance does not guarantee future performance. The article does not constitute investment advice.

Global equity markets have shown remarkable resilience in recent years, absorbing and then shrugging off shocks from the pandemic, as well as wars and policy brouhahas.

Despite punchy valuations, US equities have led the way in 2025 and continue to rise. It has certainly been a year for the record books. When Nvidia and Microsoft became the first and second firms ever to be valued at US $4 trillion, they were each deemed to be more valuable than the FTSE 100. Nvidia has since gone on to be the world’s first US $5 trillion company.

Yet, beneath the surface, a growing number of investors are starting to question whether a major market correction is brewing. Several converging themes are driving this sentiment including the rapid rise of artificial intelligence (AI), elevated gold prices, highly concentrated US equity markets, persistent inflation and uncertain interest rate trajectories in major economies, as well as an increasingly complex geopolitical backdrop.

A range of industry participants have recently spoken out. Last month, Kristalina Georgieva, Head of the International Monetary Fund, cautioned that any sharp correction in AI sentiment and therefore equity markets, “could drag down world growth, expose vulnerabilities and make life especially tough for developing countries[1].”

Similarly, Jamie Dimon, the JP Morgan CEO, questioned the extent to which AI-related trades will reward those who have invested. In his words: “The level of uncertainty should be higher in most people’s minds than what I would call normal[2].”

As the murmurings of a potential stock market correction grow, where does the truth lie? In the following article, we explore key factors behind the bearish investor sentiment in some (but not all) quarters. We also explain the nature of a market correction and discuss why it needn’t be a source of panic.

AI: Hype and hope but at what cost?

It is estimated that as much as US $1.5 trillion will have been spent on AI in 2025, with that number forecast to top $2 trillion in 2026[3].

Investor capital has flowed heavily into a handful of tech giants, but this insatiable investor appetite has created an extreme concentration in equity markets, where a few names now carry outsized influence.

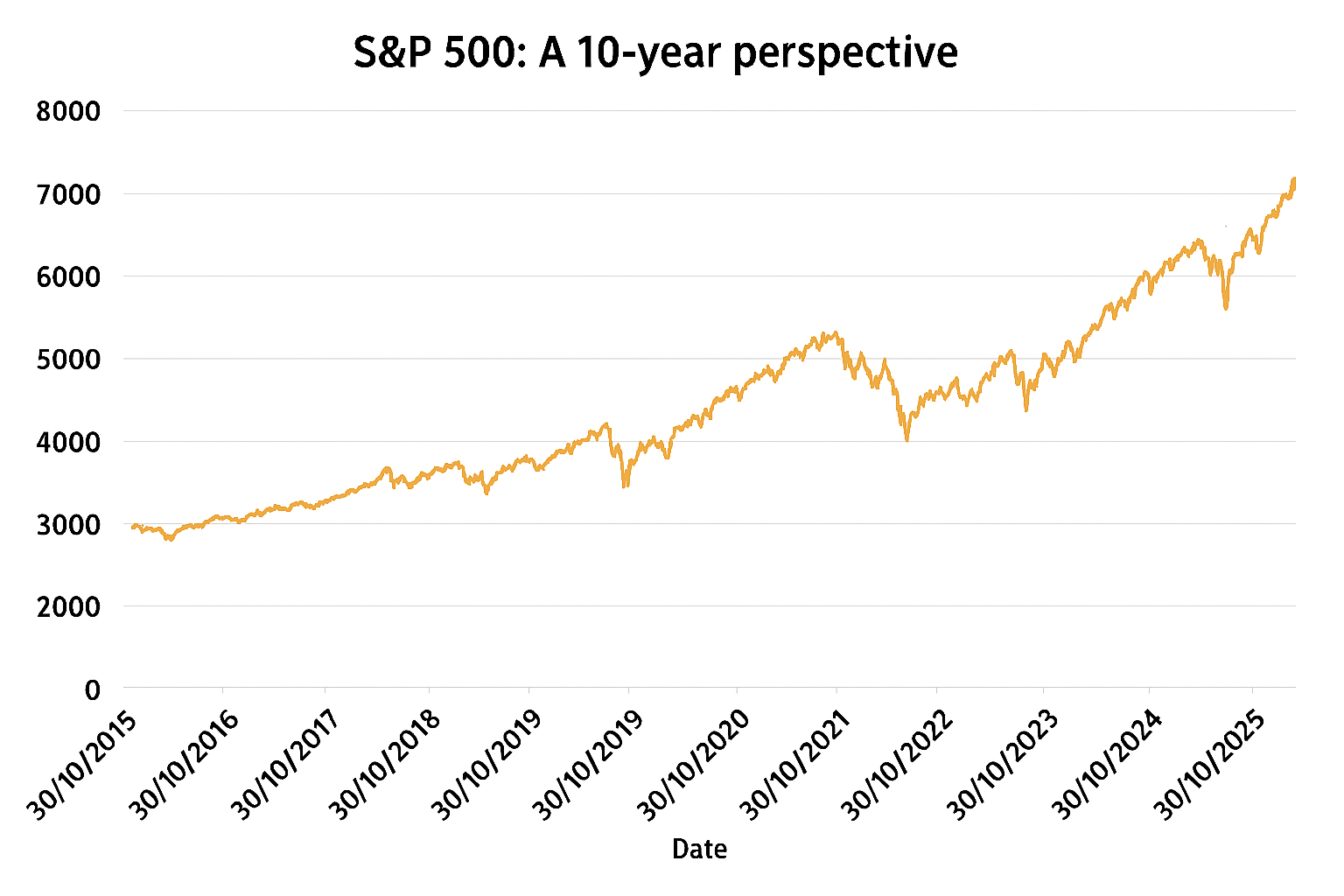

To help bring this to life, let’s consider the tech-heavy S&P 500. So far this year, the US index is up 16.6%[4] (as at 5 November 2025, starting from 2 January, and in US dollar terms). But if you remove the contribution of the Mag-7, then it’s only up 13.58%.

This extraordinary degree of influence represents a major fragility in markets. In the event of investor sentiment turning, or corporate earnings disappointing, this small basket of stocks could have a large ripple effect across entire indices. And when market breadth narrows, the risk of a sharp reversal grows.

In parallel, pessimists have pointed to the fact that a lot of investment in AI infrastructure is being funded via debt. Oracle, one of the biggest AI players, recently looked to bond markets for US $18 billion to help finance the data centre infrastructure needed for its AI ambitions[5]. In the event of a market bubble bursting, huge sums of debt could very quickly look unsustainable, exacerbating the problem.

To be clear, the above is not a prediction of what will happen. Rather, it’s an attempt to frame certain schools of thought, and to help contextualise what’s feeding some of the more pessimistic headlines that we’re currently seeing.

Gold: An alarm bell too loud to ignore?

When viewed in isolation, the recent performance of gold could be seen as a red flag for investors.

Traditionally considered a ‘safe haven’ asset, its rapid rise to record highs suggests investors are hedging en masse against uncertainty. Central banks have also been in buying mode as part of efforts to diversify away from a weakening US dollar.

Since the start of the year, the price per troy ounce of the precious metal has soared by 56%, based on a low of US $2,669.00 on 2 January 2025, to a high of $4,359.40 on 19 October 2025[6].

October also saw a price spike for silver, further indicating the flight-to-safety currently playing out. On 12 October, the price per ounce of silver (US $53) was 85% higher than at the start of the year[7].

Further signs of investor nerves emerged in mid-October, with the news that the VIX - commonly known as a Wall Street ‘fear index’ - had reached a 6-month high[8]. The catalyst was a fear of contagion across US banks amid two large bankruptcies in the domestic auto sector that exposed questionable lending activity.

Despite adding fuel to the fire for market pessimists, those contagion concerns appear to have abated, for now.

In the latter stages of October, gold dropped in value as the rush-to-buy seemingly ran out of steam. The end of Diwali in India, which remains the world’s second largest consumer of the precious metal, was cited as one of the core reasons.

Inflation, rates, geopolitics, and trade tensions

Overlapping everything that we’ve mentioned so far is the fact that inflation remains sticky in many economies. In 2025, an uneven global picture of rates and monetary policy has emerged.

This environment of higher-for-longer rates and uncertain rate trajectories challenges equity valuations and the skill of stock pickers, particularly for growth stocks whose earnings are further out on the horizon.

Angry trade dynamics have disrupted global growth prospects in 2025, as well as corporate profitability, particularly for firms with international exposure.

As we’ve said in previous articles, markets will always beat to the rhythm of their own drum. To that end, short-term political spats, as uncomfortable as they might be to watch, should not influence long-term investment strategy.

The recent thawing in US-China trade relations also bodes well for the global economy.

Historical perspective: Corrections and recoveries

All of which brings us to the broader theme of market corrections and market recoveries.

While it’s impossible to predict market events, it would be logical to assume that at some stage in the near to medium term, markets will experience a re-set.

As we said in our recent article - Are we in a tech bubble? - the hype around AI will likely moderate and a cooling in sentiment would feed into markets. Whether that’s in the form of a big or a small correction, remains to be seen.

On a broader level, it is important to understand that market corrections are not abnormal for long-term investors. Yes, the big ones can be temporarily painful. And yes, they can feel unsettling in the heat of the moment. However, you might be surprised by how frequent corrections have historically been. In some cases, the bounce back has also been relatively quick.

To better understand this, let’s consider the S&P 500 – one of the most followed stock indices in the world – and the volume of market drawdowns.

Did you know?:

· A double-digit drawdown is when the market declines by 10% or more from peak to trough. Since 1950, there have been 12 double-digit drawdowns across the S&P 500.

· Over the same time period, we’ve seen bear markets - defined as market declines of 20% of more - once every 7 years.

· When the outbreak of the COVID-19 pandemic caused a violent reaction across global markets, the S&P 500 took just 6 months to recover from the 34% drop it experienced from its pre-peak crash.

· On the flip side, however, the recovery from the dotcom crash took 7 years to reach its pre-crash peak again.

· Similarly, the peak-to-trough-to-peak recovery from the GFC slump took approximately five and a half years.

The point being that it is inevitable that a long-term investor will experience some form of stock market correction, or corrections, during their investment journey. Such events can be uncomfortable, but they don’t last forever.

When they do occur, the danger comes when investors are:

1) either overly exposed to one particular market, asset, sector, or theme.

2) trying to time the market either in the hope they will sell before a dip, and/or buy after a dip.

The cold reality is that it is almost impossible, even for professionals, to time a market with razor sharp accuracy. That is why the adage about the importance of ‘time in the market, rather timing the market’ is a good one to keep in mind whenever conditions become choppy. Maintaining a diversified portfolio or fund will typically help to weather the shock of a downturn or correction.

For additional context, all of our core investment strategies currently maintain a small cash holding within them. This means that in the event of a dip, we would in theory have some dry powder to re-allocate should we identify a good buying opportunity. And even if we don’t redeploy that cash, holding cash is a form of diversification and protection should stock markets turn.

In summary

The current environment is undoubtedly complex, with several factors contributing to equity market highs, as well as investor nerves.

Nascent tech and investor exuberance tend to make for a rocky relationship. Given the nature of investing, it is realistic to expect that record-high stock markets and the AI fever that’s feeding them, will experience a correction of some form.

Independent of today’s conditions, attempts to anticipate a correction leave investors facing a threefold problem: the inability to know when any correction will take place; the inability to know how sharp any correction could be; and the inability to know how long any correction might run for.

The goal, as always, should be to avoid panicking, to avoid panic selling, and be conscious that markets are often difficult to predict. Your long-term wealth is better protected when you stay invested, rely on diversification and your Investment Manager doing their jobs, and see market corrections for what they are – temporary dips.

This is the time for calm heads and a long-term perspective. Anything else is simply counterproductive. And if you do want to discuss in more detail, then your Adviser is always happy to help.

[1] Source: Financial Times, ‘IMF and BoE warn AI boom risks ‘abrupt’ stock market correction’, 8 October 2025

[2] Source: https://www.msn.com/en-us/money/savingandinvesting/jamie-dimon-is-worried-about-a-stock-market-correction/ar-AA1O8goE?ocid=BingNewsSerp

[3] Source: https://www.gartner.com/en/newsroom/press-releases/2025-09-17-gartner-says-worldwide-ai-spending-will-total-1-point-5-trillion-in-2025

[4] Source: https://www.spglobal.com/spdji/en/indices/equity/sp-500/?currency=USD&returntype=T-#overview

[5] Source: https://www.ft.com/content/4e39d081-ab26-4bc2-9c4c-256d766f28e2

[6] Source: https://www.msn.com/en-nz/money/watchlist?tab=Related&id=auvwoc&ocid=ansMSNMoney11&duration=Ytd&src=b_secdans&relatedQuoteId=auvwoc&relatedSource=MlAl

[7] Source: https://www.ft.com/content/e1eb2205-bba5-4b66-888b-e7e5d6dc45f4

[8] Source: https://www.ft.com/content/e6cd65b5-a70b-467e-9a93-6c484afb18bf

Photo credit: Unsplash